Q: What do a doormat and a bull-in-a-china-shop have in common? A: Neither are good approaches to negotiation. In a previous post I briefly discussed contract negotiations. Because this is something that can greatly influence one’s career, I feel it’s …

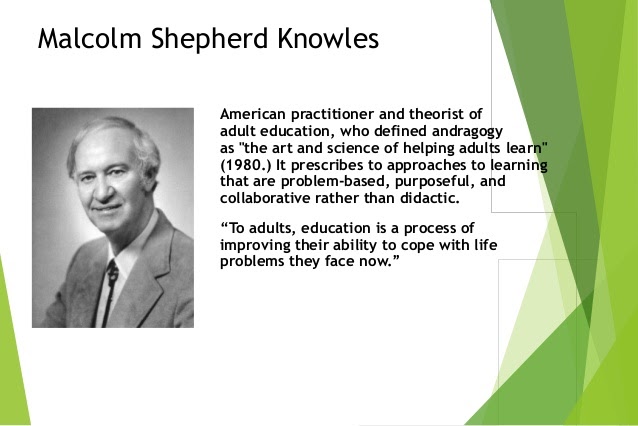

What are adult learning principles? What does it mean to apply “adult learning principles” to one’s teaching? Are you already doing it? If you don’t know the answers to these questions I invite you to keep reading. Research that looks …

Radiologists can relate to the phrase “a picture is worth a thousand words.” “The only constant is change” is another adage perfectly describing the specialty. And this dictum was hammered home by faculty throughout my radiology training: “If it isn’t …

If you are a radiology resident or fellow or you are a medical student interested in pursuing radiology, you should know that there are a gazillion opportunities for you to become actively involved in radiology societies and benefit from a …

I’m guessing that most of you have been inundated with presenting or watching webinars during this time when many face-to-face conferences have been canceled or made virtual. You probably have a few pet peeves about some of the webinars you’ve …

One of the most popular posts on The Reading Room is about radiologist compensation (FYI: it’s worth clicking on the link for the title of said blog post alone). Alas, as money still doesn’t grow on trees, it seemed like …

They tumble, slide, jump, soar. They get the jitters and often seem moodier than a hormone-addled teenager. They are the stuff of which dreams are made—the rise and fall of fortunes in mythological proportions. I’m thinking of how fortune smiled …

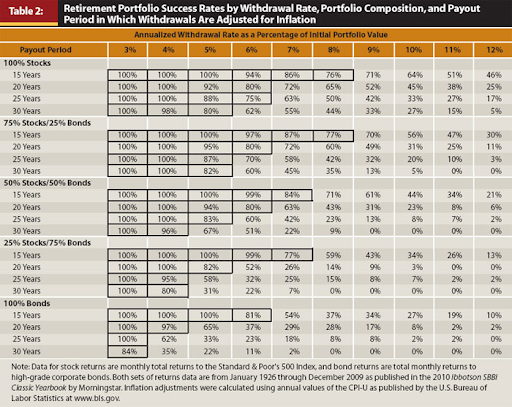

“I want the last cheque I write to bounce.” Chuck Feeney Ah, the golden years—riding into that retirement sunset. For some, it’s an eagerly-anticipated time in life, filled with big dreams; possibly, plans of moving to Florida. For others, shudder-the-thought. …

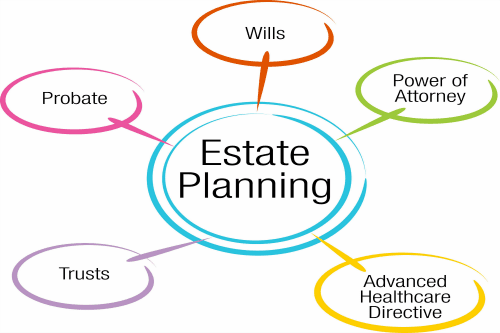

If you’re looking for a barrel of laughs, you should probably read something else; if you’re looking for practical advice on how to ensure your “affairs” are “in order” before you “croak,” you’re in the right place! And if you’re …

The term “estate” is commonly defined as a vast piece of property owned by a prominent family. As in, William Pumpernickel of the Pensicola Pumpernickels invites you to his country estate for croquet and crumpets. For purposes of this post, …